Cast Bars

Cast Bars  Minted Coins

Minted Coins  Minted Tablets

Minted Tablets  Granules

Granules  Custom Coins & Bars

Custom Coins & Bars December 2015 Commentary

December 2015 Commentary

Gold

What a difference 6 weeks can make in the gold market! After threatening to break up through the USD1200/oz level at the end of October, by the first week of December it was looking like a break down through USD1050 was on the cards. This volatility in gold (and indeed all the precious metals) is probably more a function of the speculators in the market trying to guess the effect of the first interest rate hike since 2006 in the US rather than a reflection of any real underlying demand and supply functions.

Probably the best thing that can happen now is to get the first one out of the way and see what the rhetoric from the Fed about the subsequent strategy from here on implies. The problem as the market sees it isfor the in the second part of the equation, how fast will the Fed increase rates to a more “normal” level? The answer, however, is not really in the timing at all but in the end result and the final level at which they will stop raising. Realistically, the interest rate cycle is always a moving feast but the impact on investors and hedge funds in particular is undeniable; a rising interest rate market makes interest rate bearing products more attractive and makes funding speculative gold positions more expensive and this is not viewed to be good for gold. That being said, the next question then becomes how much is already built into the price.

The net open positions in the futures contracts have built up again after reducing during the recent rally. This implies that the speculators are re-building net short positions looking for lower levels. This will have the effect of cushioning any further sell-off as profit-taking steps in.

The Indian refiners continue to be inundated with dore as the incentive scheme provided by the government there drags more and more primary gold towards that country. Having said that, it is difficult for the accredited refineries to keep up with the inflow and hence we are finding out first hand that the preference is still to give this metal to LBMA accredited refiners, such as ourselves, rather than risk a potential default on payment just to attain a better refining rate.

Technical analyses, meanwhile, place the pull-back level for the run up we have had in US gold since the early 2000’s at around $970/oz. This is a level that will strike fear into some of the struggling North American producers whose costs at some mines are already exceeding the current price levels. Maybe it is for exactly this reason that the gold price needs to move to a lower price to remove some marginal supply and restore some sort of equilibrium back into the supply/demand model which has relied far too much on continually increasing investor flows to soak up the ongoing supply of gold.

In all, 2016 could be an interesting year for the gold market.

\

\

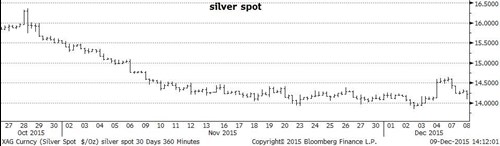

Silver

Silver made a valiant attempt at the topside as gold was getting some relief from its selling spree in early December, but eventually succumbed to the overall precious metal selling pressure. As predicted, however, the sub-USD14.00/oz level was well supported and the long ETF holders continued to back their silver positions and resisted the temptation to liquidate substantial holdings.

Imports into India have been running at all-time highs and at times it seems there is some advantage to being gold’s poorer (and cheaper) cousin. Demand for silver bars and coins also remains fairly buoyant and some of its allure as an industrial metal is appearing back in commentaries as the U.S. is (hopefully) dragging itself back into a growth phase for its economy. The ultimate hope, of course, is that this will pull the global economy back onto a positive frame of mind as well.

Additionally, China seems to be settling down somewhat after the turbulent time its stock markets have had and the general weakness in commodity prices across the board. The market spectators seem to be coming to grips with the idea now that China’s growth rate is moderating but that percentage increases on a larger base still generate big numbers in terms of overall volumes.

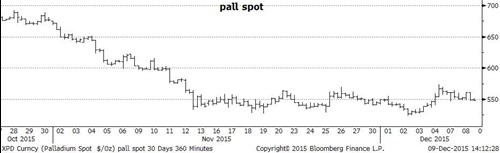

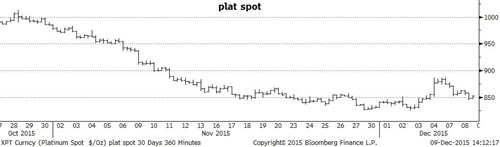

Platinum and Palladium

The downward spiral for platinum and palladium prices continued with both the US900 level in platinum and the US600 level in palladium giving way.

Speculative shorts continue to pound these markets and as the VW scandal support largely dissipated, it left the downside open to be tested.

It appears that both markets have found some firmer footing now, however with platinum bouncing off the US825 floor and palladium reversing at around US525/oz.

Platinum’s discount to gold has moved down to over $220/oz which is the largest discount platinum has ever had to gold in recorded market history. The fact that 70% of mine production in South Africa is underwater as far as profitability is concerned also continues to be ignored although the stronger USD and weaker Rand is probably providing some sort of a buffer against this reality. Perhaps the only event to change this mentality will be the actual closure of a mine or platinum mining company, but again, this is a political football that may be kicked around for some time yet.

Meanwhile, with production continuing at a steady pace (and at higher levels than last year) there is nothing to persuade the end-users of the metal to buy any more than is required to fill current orders. There is also no empirical evidence showing a lack of physical availability so there are currently no fears of a squeeze.

This could, however, change very quickly.

Palladium has had much the same flight path as platinum over the last couple of weeks although it seems to be a little better supported at the lower levels than its compadre. The size of the short position and the length of time it has been held is probably assisting to support it as profit-taking emerges combined with the doggedness of some long-holders who are still willing to add at the lower levels as well.

The support that palladium received from the VW scandal as the market predicted an increase in the demand for petrol powered cars (which largely use palladium for their catalytic converters), has also subsided to a large extent.

The ability for it to hold these lower levels, however, does augur well for a rally early in the new year bearing in mind the still significant short position held by the speculators in this market.